Let’s Talk About Your Insurance Needs

Have questions or need a specialized insurance quote?

Our team is ready to help you find the right insurance for your business. Our specialists are great at listening to your needs and offering expert advice to help you find the right coverage! We work with businesses from all of the major US industries and are ready to assist you today!

We're here to help! Reach out to us by phone, text or email. Our team is here from Monday through Friday, 9:00 AM to 5:30 PM (Pacific Time).

We’d love to hear from you - Give us a call at - 971-412-4471

Contact Us

How to Read & Understand a Certificate of Insurance

A contractor-friendly guide to understanding your COI, checking coverage limits, reviewing certificate holders, and spotting common problems before they delay a job.

What Is a Certificate of Insurance

A COI is evidence of insurance

It summarizes certain policies and limits

It is not the insurance policy itself

It generally does not create coverage by itself

The actual policy forms and endorsements control coverage

The 15 Parts of a COI Every Contractor Should Understand

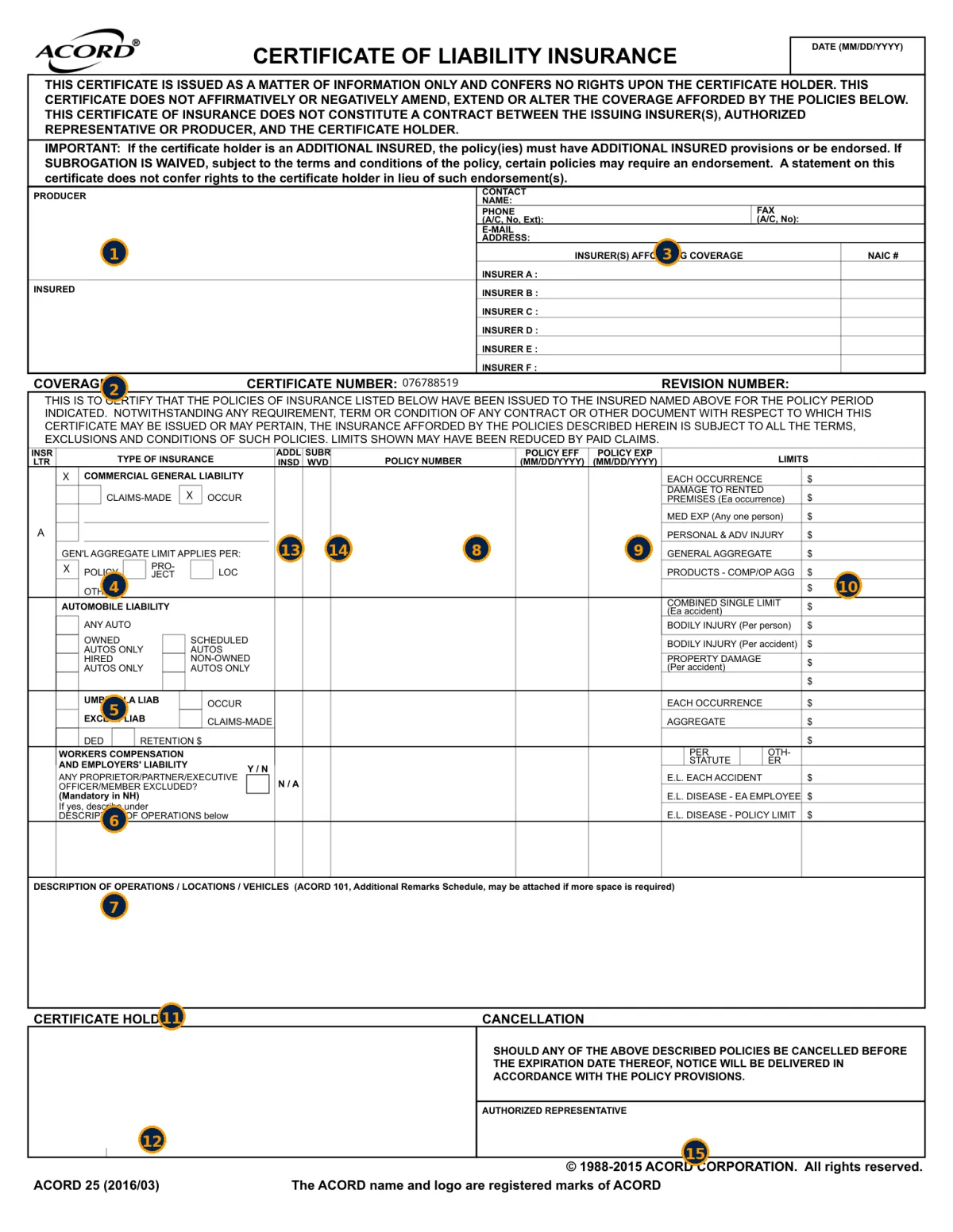

① Producer

BROKER

① The insurance agency or broker issuing the certificate.

② Insured

BUSINESS

② The business or individual shown as the named insured.

③ Insurers Affording Coverage

INSURER'S

③The insurance companies providing the policies shown.

④ General Liability

INSURANCE

④ General Liability

⑤ Auto Liability

⑥ Umbrella / Excess Liability

⑦ Workers Compensation

⑧ Policy Numbers

POLICY NUMBERS

The identifying numbers for each policy.

⑨ Effective & Expiration Dates

DATES

The dates coverage is scheduled to remain active.

⑩ Coverage Limits

LIMIT

The maximum limits shown for each listed policy.

⑪ — Description of Operations

ENDORSEMENTS

Where project information and references to certain endorsements or requirements may appear.

⑫ Certificate Holder

HOLDER

The identifying numbers for each policy.

⑬ Additional Insured Indicators

ADDED INSUREDS

The identifying numbers for each policy.

⑭ Subrogation Waiver

WAIVER

The identifying numbers for each policy.

⑮ Authorized Representative

BROKER

The identifying numbers for each policy.

How Do I Read a COI?

Use the chart below to reference each part

Find It on the Certificate

①–③ Who’s Involved

Producer, insured business, and insurance companies.

④–⑦ Coverage Types

General Liability, Auto, Umbrella/Excess, and Workers’ Compensation.

⑧–⑩ Policy Details

Policy numbers, dates, and listed limits.

⑪–⑮ Requirements & Recipients

Operations descriptions, certificate holder information, coverage indicators, and representative details.

⑧ — Policy Numbers

POLICY NUMBERS

The identifying numbers associated with each listed policy.

⑨ — Effective & Expiration Dates

DATES

The dates coverage is scheduled to begin and expire.

⑩ — Coverage Limits

LIMITS

The maximum limits shown for each listed policy, subject to policy terms.

⑪ — Description of Operations

PROJECT DETAILS

Where project information and references to certain endorsements or requirements may appear.

⑫ — Certificate Holder

HOLDER

The organization or person receiving evidence of insurance.

⑬ — Additional Insured Indicators

ADDITIONAL INSURED

Areas that may indicate additional insured status, subject to actual policy terms and endorsements.

⑭ — Subrogation Waiver Indicators

WAIVER

Areas that may indicate whether a waiver of subrogation applies, subject to policy provisions and endorsements.

⑮ — Authorized Representative

REPRESENTATIVE

The authorized representative section associated with issuance of the certificate.

Certificate Holder Vs. Additional Insured

Certificate Holder vs. Additional Insured

— Certificate Holder

Receives Evidence of Insurance

Being listed in the Certificate Holder box generally identifies who is receiving the certificate. It does not automatically mean that organization is an additional insured.

— Additional Insured

Coverage Status Depends on Policy Terms

Additional insured status generally depends on applicable policy wording, endorsements, and sometimes written contract requirements.

Important: A company appearing in the Certificate Holder box is not automatically an Additional Insured.

Why Was My COI Rejected?

Incorrect Certificate Holder

The legal name or address may not match submitted requirements.

Missing Coverage Requirement

The requesting organization may require coverage not shown on the certificate.

Required Endorsement Issue

A contract may call for additional insured, waiver, or other endorsement wording.

Expired Policy Dates

The certificate may show a policy term that has expired or is approaching expiration.

Insufficient Limits

Required limits may exceed those shown.

Auto Coverage Mismatch

The contract may require an auto coverage designation not reflected on the certificate.

Project Information Missing

Specific job, location, or contract information may be requested.

Name Mismatch

The insured business name may not match licensing or contract records.

Could a Certificate Stop Your Company From Working?

Certificate Rejected

Coverage's Affected

✓ General Liability

✓ Additional Insured Endorsements

✓ Waiver of Subrogation

✓ Primary & Non-Contributory

What Happened?

A certificate request is rejected because required endorsements or wording are missing.

Why It Matters

Certificate issues can delay project starts, create disputes with GCs, and prevent contractors from accessing jobsites.

How JCF Helps

We review contracts, endorsements, and certificate requirements before they become jobsite problems.

Nightmares

Could a rejected certificate shut down your jobsite?

Common Risks Contractors Face

Irrigation Line

Strike- Leak

Work Truck Accident

Stolen Excavator

OSHA Worker Injury

Certificate Emergency

Bond

Rejected

Burst Pipe

Flood Claim

Overnight

Rainstorm

The Shattered

Installation

Uninsured Subcontractor

Hot Work Fire

Claim

HVAC Refrigerant Leak Claim

Questions About Certificates of Insurance?

Certificates of Insurance can be confusing—especially when contracts include requirements involving Additional Insured status, Waivers of Subrogation, specific liability limits, Commercial Auto coverage, or project-specific endorsements. These frequently asked questions explain some of the most common COI issues contractors encounter.

Common questions answered

Answers to Frequently Asked Questions

What is a Certificate of Insurance?

A Certificate of Insurance, commonly called a COI, is a document that provides a summary of certain insurance policies, coverage types, policy dates, and limits shown at the time the certificate is issued.

Contractors are often asked to provide a COI to general contractors, project owners, property managers, landlords, municipalities, and other organizations before beginning work.

A COI is an important form of evidence of insurance, but it is not the insurance policy itself. Actual coverage is determined by the underlying policies, forms, endorsements, exclusions, and conditions.

Is a COI proof of insurance?

A COI is commonly used as evidence that certain insurance policies and limits are shown as in effect on the date the certificate is issued. However, it does not replace the actual insurance policy or guarantee that every contractual insurance requirement has been satisfied.

For example, a certificate may show General Liability coverage and policy limits, but that alone may not confirm the full scope of coverage, all exclusions, or whether a specific organization has Additional Insured status.

The underlying policy and applicable endorsements control actual coverage.

Is a Certificate Holder automatically an Additional Insured?

No. Being listed as a Certificate Holder does not automatically make a person or organization an Additional Insured.

The Certificate Holder is generally the person or organization receiving the certificate as evidence of insurance. Additional Insured status is different and generally depends on the terms of the policy, applicable endorsements, and sometimes the requirements of a written contract.

This is one of the most common misunderstandings contractors encounter when submitting Certificates of Insurance.

What does $1 million / $2 million mean on a COI?

When someone refers to $1 million / $2 million General Liability limits, they are commonly referring to:

$1,000,000 Each Occurrence

$2,000,000 General Aggregate

The Each Occurrence limit generally refers to the maximum amount shown for a covered occurrence, subject to policy terms. The General Aggregate generally refers to the maximum amount shown for certain covered claims during the applicable aggregate period.

A COI may also display separate limits for Products-Completed Operations, Personal and Advertising Injury, Damage to Rented Premises, and Medical Expense.

The exact application of these limits depends on the policy terms and circumstances of a claim.

What is the Description of Operations box on a COI?

The Description of Operations / Locations / Vehicles section is an area of the certificate where additional information may be included about a project, location, contract, certificate holder requirement, or certain insurance provisions. For contractors, this section may contain references to items such as:

- Project names or job numbers

- Specific work locations

- Additional Insured provisions

- Primary and Noncontributory wording

- Waiver of Subrogation

- Completed Operations

- Applicable endorsements

However, wording placed in the Description of Operations box does not automatically create or change insurance coverage. Actual coverage depends on the underlying policy and applicable endorsements.

What is the difference between a COI and an insurance policy?

A Certificate of Insurance is a summary document used to provide evidence of certain insurance information. An insurance policy is the actual contract that contains the coverage agreements, definitions, exclusions, conditions, limits, forms, and endorsements that determine coverage.

A COI may show that a contractor carries General Liability, Commercial Auto, Umbrella, or Workers’ Compensation insurance, but it does not reproduce the complete terms of those policies.

When there is a question about whether a particular claim, project, organization, or contractual requirement is covered, the actual policy and applicable endorsements control—not the certificate alone.

What does Additional Insured mean?

An Additional Insured is a person or organization that may receive certain coverage under another party’s insurance policy, subject to the policy language and applicable endorsements.

Contractors are frequently required by written contracts to provide Additional Insured status to parties such as:

General contractors

Project owners

Property managers

Landlords

Developers

Other contracting parties

The scope of Additional Insured coverage can vary. It may depend on factors such as ongoing operations, completed operations, written contract requirements, and the specific endorsement attached to the policy.

Simply listing a company as a Certificate Holder does not automatically provide Additional Insured status.

What is a Waiver of Subrogation?

A Waiver of Subrogation is a policy provision or endorsement that may limit an insurance company’s ability to pursue recovery from a specified party after paying a covered claim, subject to the policy terms and applicable endorsement.

Contractors may encounter Waiver of Subrogation requirements in agreements with:

General contractors

Project owners

Developers

Landlords

Property managers

Other contracting parties

A checkmark or reference on a COI may indicate that a waiver applies, but the actual policy language and endorsement determine whether and how the waiver is provided.

Why was my Certificate of Insurance rejected?

A Certificate of Insurance may be rejected when the information shown does not match the requesting party’s insurance requirements.

Common reasons include:

- Incorrect Certificate Holder name or address

- Insufficient liability limits

- Missing Additional Insured requirements

- Missing Waiver of Subrogation

- Missing Primary and Noncontributory requirements

- Required Completed Operations coverage not addressed

- Commercial Auto requirements not satisfied

- Umbrella or Excess Liability limits not shown

- Expired or incorrect policy dates

- Incorrect named insured

- Missing project or location information

- Required endorsements not provided

If your COI is rejected, obtaining a copy of the exact insurance requirements can help your insurance agent determine what is being requested and whether your existing policies can satisfy those requirements.

Can an insurance agent change a COI to meet contract requirements?

An insurance agent generally cannot simply change a Certificate of Insurance to create coverage that does not exist.

For example, if a contract requires higher liability limits, Additional Insured status, a Waiver of Subrogation, Primary and Noncontributory wording, or a particular type of Auto Liability coverage, the underlying insurance policy may need to already provide that coverage or be properly endorsed.

Depending on the requirement, changes could involve:

- Adding an endorsement

- Increasing policy limits

- Modifying coverage

- Adding another policy

- Obtaining carrier approval

- Paying additional premium

- Confirming that the existing policy already satisfies the requirement

The COI should reflect applicable insurance information; it should not be used to manufacture coverage that the policy does not provide.

Does a COI show all policy exclusions and coverage conditions?

No. A Certificate of Insurance does not normally show every exclusion, limitation, endorsement, condition, classification, or coverage restriction contained in an insurance policy.

A COI is a summary document. Important policy provisions may exist that are not visible on the certificate, including:

- Coverage exclusions

- Classification limitations

- Designated work exclusions

- Residential construction restrictions

- Height or depth limitations

- Subcontractor requirements

- Geographic limitations

- Professional services exclusions

- Roofing or exterior work restrictions

- Other policy-specific conditions

This is why a COI should not be treated as a complete substitute for reviewing the actual insurance policy and applicable endorsements.

Get a Contractor Insurance Quote

Whether you're a new contractor or reviewing your current coverage, we can help you

compare options and identify potential coverage gaps.

Contact Us

(971) 412-4469

9020 SW Washington Sq Rd Portland, OR 97223

Website

Facebook

Instagram

LinkedIn