🏛 Contractor Knowledge Academy

Lesson 1: Why General Contractors Require a Certificate of Insurance

Estimated Reading Time: 6 minutes • Last Updated: July 2026

🏛 Contractor Knowledge Academy

Lesson 1: Why General Contractors Require a Certificate of Insurance

Estimated Reading Time:

6 minutes • Last Updated: July 2026

COI-101

COI

Why General Contractors Require a Certificate of Insurance Before Work Begins

Why General Contractors Require a Certificate of Insurance Before Work Begins

Add a Title Here

Welcome to the Contractor Knowledge Academy

Whether you're a new contractor or you've been in business for decades, understanding insurance requirements

can help you avoid costly mistakes, keep projects moving, and win more work.

Each lesson is designed to answer common contractor questions using real-world examples and practical guidance—not insurance jargon.

ACADEMY Lesson

#1 of 10

"Please send us your Certificate of Insurance."

COI-101

Small Call to Action Headline

For many contractors, it's just another piece of paperwork. In reality, it's one of the most important documents on a construction project.

A Certificate of Insurance (COI) helps general contractors verify that subcontractors meet the insurance requirements outlined in the contract. Without an approved certificate, work may be delayed, payments can be held up, or you may not be allowed on the jobsite.

Understanding why contractors request Certificates of Insurance—and what they're actually reviewing—can help you avoid unnecessary delays and keep your projects moving.

For many contractors, it's just another piece of paperwork. In reality, it's one of the most important documents on a construction project.

A Certificate of Insurance (COI) helps general contractors verify that subcontractors meet the insurance requirements outlined in the contract. Without an approved certificate, work may be delayed, payments can be held up, or you may not be allowed on the jobsite.

Understanding why contractors request Certificates of Insurance—and what they're actually reviewing—can help you avoid unnecessary delays and keep your projects moving.

What Is a Certificate

of Insurance?

What Is a Certificate of Insurance?

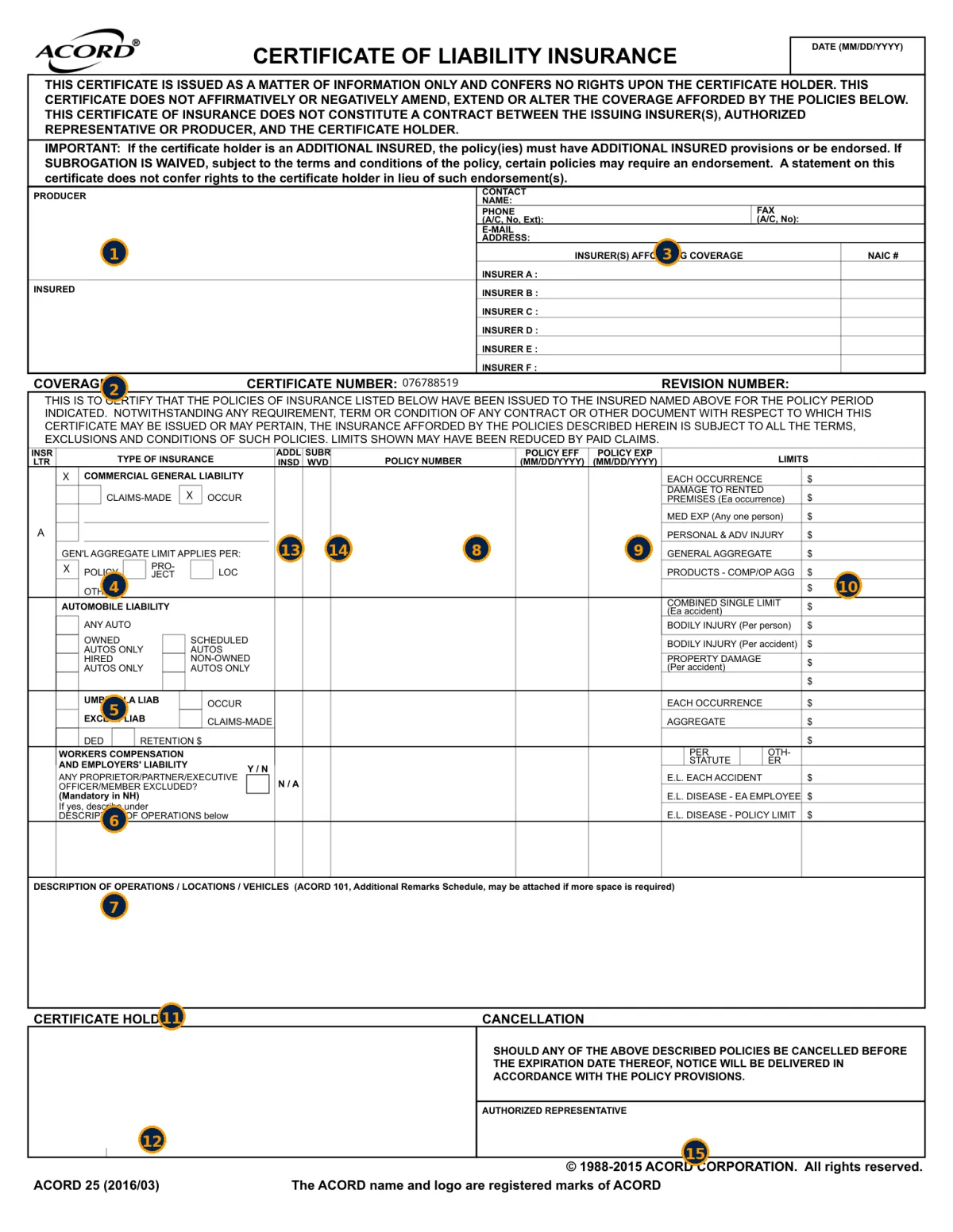

A Certificate of Insurance (COI) is a document that summarizes your insurance coverage at the time it is issued. Most Certificates of Insurance are created using the industry-standard ACORD 25 form.

A Certificate of Insurance (COI) is a document that summarizes your insurance coverage at the time it is issued. Most Certificates of Insurance are created using the industry-standard ACORD 25 form.

A Typical COI Includes:

- Named Insured

- Insurance Company Information

- Policy Numbers

- Effective and Expiration Dates

- Coverage Types

- Policy Limits

- Certificate Holder

- Description of Operations

👉 Want to understand every section?

Read our Complete Certificate of Insurance Guide. (Internal Link)

While it provides evidence that insurance exists, a COI is not the insurance policy itself. It does not change, expand, or replace the terms of your policy.

A Typical COI Includes:

- Named Insured

- Insurance Company Information

- Policy Numbers

- Effective and Expiration Dates

- Coverage Types

- Policy Limits

- Certificate Holder

- Description of Operations

👉 Want to understand every section? Read our Complete Certificate of Insurance Guide. (Internal Link)

While it provides evidence that insurance exists, a COI is not the insurance policy itself. It does not change, expand, or replace the terms of your policy.List item 1

What Are General Contractors Actually Looking For?

Many contractors believe the general contractor simply wants proof that insurance exists.

In reality, they may review several important details before approving your certificate.

They often verify:

- General Liability limits

- Commercial Auto coverage (when required)

- Workers' Compensation coverage

- Umbrella or Excess Liability limits

- Policy effective dates

- Insurance carrier information

- Certificate Holder details

- Required endorsements

Depending on the project, they may also require:

- Additional Insured status

- Waiver of Subrogation

- Primary & Non-Contributory wording

- Completed Operations coverage

Each construction contract is different, which is why insurance requirements can vary from one project to another.

Common Reasons Certificates Get Rejected

A rejected Certificate of Insurance doesn't always mean you have poor insurance.

Sometimes it's simply missing required information. Some of the most common reasons include:

❌ Incorrect certificate holder

❌ Expired policy

❌ Missing Additional Insured endorsement

❌ Coverage limits below contract requirements

❌ Missing Waiver of Subrogation

❌ Missing Primary & Non-Contributory wording

❌ Incorrect business name

❌ Incorrect policy information

❌ Missing Completed Operations coverage

Even small errors can delay project approval until a corrected certificate is submitted.

What Happens If You Can't Provide

an Approved COI?

Depending on the contract, you could experience:

Delayed project start dates

Jobsite access denied

Delayed payments

Contract compliance issues

Additional administrative costs

Removal from an approved subcontractor list

Having the right insurance is important—but providing accurate documentation is just as important.

Beyond the Certificate

A Certificate of Insurance is only a snapshot of your coverage.

General contractors often require endorsements that

cannot be confirmed by the certificate alone.

That's why it's important to understand not only what your COI says—but also what your insurance policy actually provides.

If you're unsure whether your coverage meets contract requirements, review your policy with your insurance professional before work begins.

Contractor Knowledge Tip

A Certificate of Insurance Doesn't Create Coverage

One of the biggest misconceptions in construction is that a Certificate of Insurance changes your policy.

It doesn't.

A COI simply summarizes the insurance that exists on the date it was issued.

If your contract requires Additional Insured status, Waiver of Subrogation, or other endorsements, those protections typically need to exist within your insurance policy—not just be listed on the certificate.

Common Reasons

Certificates Get Rejected

A rejected Certificate of Insurance doesn't always mean you have poor insurance.

Sometimes it's simply missing required information. Some of the most common reasons include:

❌ Incorrect certificate holder

❌ Expired policy

❌ Missing Additional Insured endorsement

❌ Coverage limits below contract requirements

❌ Missing Waiver of Subrogation

❌ Missing Primary & Non-Contributory

❌ Incorrect business name

❌ Incorrect policy information

❌ Missing Completed Operations coverage

Even small errors can delay project approval until a corrected certificate is submitted.

What Happens If You Can't Provide an Approved COI?

Depending on the contract, you could experience:

Delayed project start dates

Jobsite access denied

Delayed payments

Contract compliance issues

Additional administrative costs

Removal from an approved subcontractor list

Having the right insurance is important—but providing accurate documentation is just as important.

Beyond the Certificate

A Certificate of Insurance is only a snapshot of your coverage.

General contractors often require endorsements that

cannot be confirmed by the certificate alone.

That's why it's important to understand not only what your COI says—but also what your insurance policy actually provides.

If you're unsure whether your coverage meets contract requirements, review your policy with your insurance professional before work begins.

Contractor Knowledge Tip

A Certificate of Insurance Doesn't Create Coverage

One of the biggest misconceptions in construction is that a Certificate of Insurance changes your policy.

It doesn't.

A COI simply summarizes the insurance that exists on the date it was issued.

If your contract requires Additional Insured status, Waiver of Subrogation, or other endorsements, those protections typically need to exist within your insurance policy—not just be listed on the certificate.

Learn More

Continue exploring the Contractor Knowledge Academy:

📘 Complete Certificate of Insurance Guide

📘 Additional Insured Explained

📘 Waiver of Subrogation Explained

📘 Primary & Non-Contributory Explained

Learn More

Continue exploring the Contractor Knowledge Academy:

📘 Complete Certificate of Insurance Guide

📘 Additional Insured Explained

📘 Waiver of Subrogation Explained

📘 Primary & Non-Contributory Explained

📘 How to Read a Certificate of Insurance

📘 Common Reasons COIs Get Rejected

Coming Next...

🚧 Contractor Nightmare

"The Contractor Who Lost a $2 Million Project Because of One Missing Endorsement."

Sometimes the difference between winning a job and losing one isn't your price—it's your paperwork.

(Internal Link when published.)

🏛 Contractor Knowledge Academy

JC Family Insurance

Need a Certificate of Insurance?

Whether you need a standard Certificate of Insurance or one that includes Additional Insured, Waiver of Subrogation, Primary & Non-Contributory wording, or project-specific requirements, JC Family Insurance can help.

🏛 Contractor Knowledge Academy | JC Family Insurance

Need a Certificate of Insurance?

Whether you need a standard Certificate of Insurance or one that includes Additional Insured, Waiver of Subrogation, Primary & Non-Contributory wording, or project-specific requirements, JC Family Insurance can help.

Common questions answered

Answers to Frequently Asked Questions

Why do general contractors ask for a Certificate of Insurance?

General contractors use Certificates of Insurance to verify that subcontractors carry the insurance required by the construction contract before work begins.

Does a Certificate of Insurance guarantee coverage?

No. It provides evidence of insurance at the time it is issued but does not guarantee coverage for every claim or situation.

Can I start work without providing a Certificate of Insurance?

Many general contractors require an approved Certificate of Insurance before allowing subcontractors to begin work on the project.

What is Inland Marine insurance?

Inland Marine covers tools, equipment, trailers, and mobile property used on jobsites.

What bonds do contractors need?

Requirements vary by state and project. Common bonds include license bonds, permit bonds, bid bonds, performance bonds, and payment bonds.

Is a Certificate of Insurance the same as my insurance policy?

No. A Certificate of Insurance summarizes your coverage but does not replace or modify the actual insurance policy.

Why was my Certificate of Insurance rejected?

Common reasons include incorrect certificate holder information, expired policies, insufficient coverage limits, or missing required endorsements.

What endorsements might a general contractor require?

Common requirements include Additional Insured status, Waiver of Subrogation, Primary & Non-Contributory wording, and Completed Operations coverage, depending on the contract.

How quickly can I get a contractor insurance quote?

Many contractor quotes can be completed the same day depending on the trade and information provided.

Do you insure high-risk contractors?

Yes. We work with many markets that specialize in roofing, excavation, framing, concrete, tree service, and other higher-risk trades.

Contact Us

(971) 412-4469

9020 SW Washington Sq Rd Portland, OR 97223

Website

Facebook

Instagram

LinkedIn